In today’s fast-paced digital world, traditional banking models are constantly changing. Banking as a service is no exception – an innovative concept fundamentally changing the financial landscape.

In this blog post, we dive deeper into the BaaS world, exploring its core principles, benefits, and real-world applications.

What is Banking as a Service

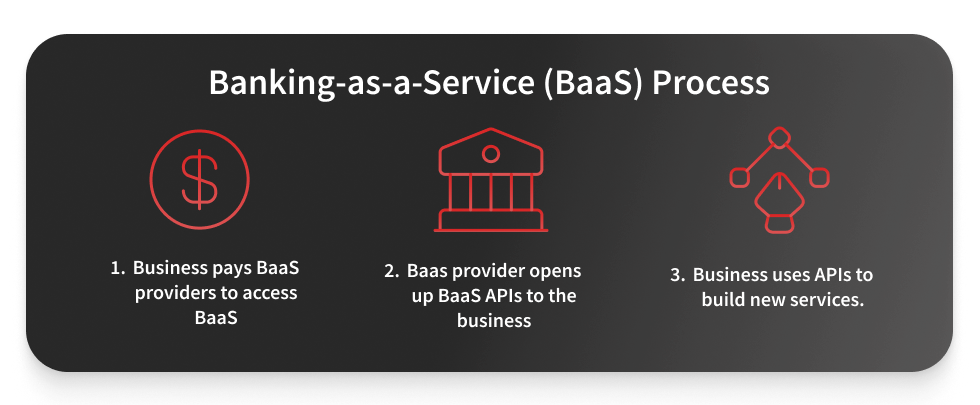

Banking as a Service (BaaS) is a start-to-finish process when traditional banks open their infrastructure and capabilities to digital banks and third-party providers. Also, it is known as embedded banking. BaaS lets integrate business infrastructure with a bank’s system via Application Programming Interfaces (APIs).

📚Related: How Open API in Banking is Driving Growth?

Licenses and regulations are a part of the banking industry. Therefore, financial institutions obtain various regulatory requirements such as anti-money laundering (AML), compliance with OFAC sanctions lists, and ensuring data privacy and security.

The integration empowers e-banks and third parties to offer complete BaaS service as part of their non-bank business offerings. In other words, this helps fintech companies, technology platforms, or non-bank businesses offer banking services directly to their customers without obtaining a banking license.

With BaaS, customers can conveniently access banking services while purchasing a product or utilizing a service. FinTech payments, product finance, loans, and credit cards are some services available through the seller’s website.

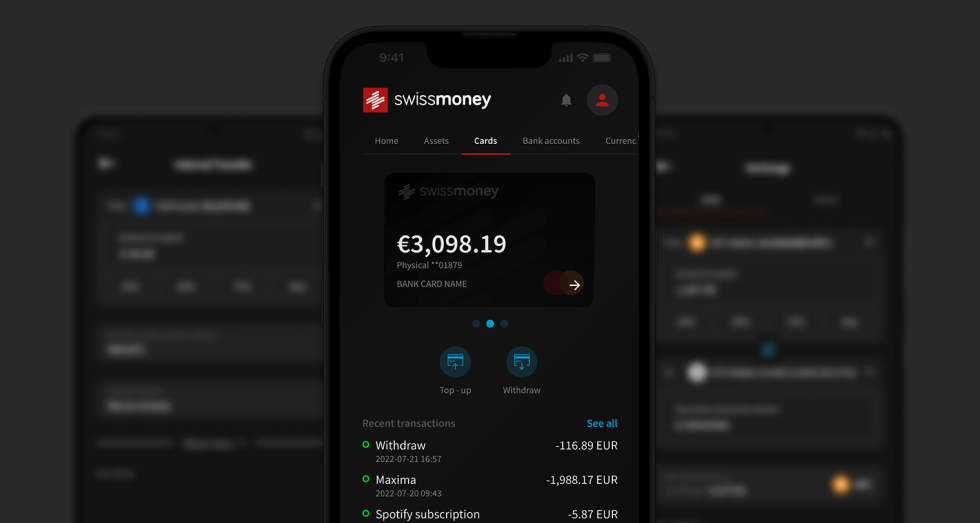

For example, swissmoney allows various businesses to open accounts online within 10 minutes. In addition to money transfers, online payments, and fast money amount increase approval, it also offers mobile wallets, online payments, and more.

Also, swissmoney offers BaaS-embedded financial services in Europe and globally.

Neobank

Neobanks are online-only financial institutions, banking platforms without physical branches or a banking license. They are categorized as non-bank fintech companies.

This kind of financial institution is among the companies that leverage banking as a service (BaaS). Neobanks focus on specific areas of banking, such as providing checking and savings accounts and issuing credit cards, rather than engaging in traditional lending activities.

By utilizing BaaS, neobanks can offer innovative financial services while relying on the infrastructure and capabilities of partnering banks.

Full-service licensed bank offers five types of banking:

- Checking and savings accounts

- Issuing credit cards to customers

- Making loans

- Overdraft protection

- Wealth management

Unfortunately, non-banks don’t offer all five types of banking.

How does BaaS work for platforms?

Banking as a Service (BaaS) provides platforms with access to banking functionalities and services. Here is how it typically works:

1. Integration

The platform forms a partnership or collaborates with a conventional bank or a BaaS provider that provides banking infrastructure and capabilities via APIs. In general, the platform links the bank’s systems and services.

2. Customization

Next, the platform adapts the banking service to fit their unique business demands and requirements. It may involve branding, modifying the user interface, and adjusting the platform banking services to fit naturally into the platform’s user interface.

3. Seamless user experience

After integration, the platform’s customers can access a range of banking services directly within the platform. It may include:

- opening a personal bank account

- making payments

- transferring funds

- applying for loans or credit cards

- managing their financial transactions

4. Regulatory compliance

The bank or BaaS provider ensures the platform complies with pertinent banking and financial regulations. It is a part of the BaaS agreement. It includes:

- implementing required security safeguards

- protecting personal data

- upholding know-your-customer (KYC) and anti-money laundering (AML) regulations

5. Revenue sharing

Whether the platform and the bank/BaaS provider can share revenues generated from the provision of banking services depends on the agreement. This BaaS model allows the platform to monetize the added value of banking services provided to customers.

BaaS and embedded finance

Embedded finance, also known as embedded banking or finance-as-a-service, refers to the integration of financial services into non-financial platforms such as e-commerce websites, mobile apps, and other digital platforms.

BaaS providers are companies that offer BaaS embedded finance services infrastructure, technologies, and capabilities) to FinTech and businesses in other industries for their customers to use. The providers usually collaborate with licensed and regulated banks directly. This partnership allows them to leverage the bank’s regulatory licenses, systems, and expertise.

Furthermore, they are responsible for regulatory aspects, data security, compliance, and technology integration. With the help of Banking as a Service service provider, companies can focus on providing banking services to their customers without setting up a full-fledged bank.

In addition, BaaS providers offer APIs (Application Programming Interfaces). This service allows non-bank businesses to integrate services into their platforms or applications and enable customers to hold funds, pay bills, manage cash flow, or use another financial service.

BaaS providers play the main role in democratizing access to banking services. It drives innovation in the financial industry and enables non-bank businesses to offer various financial offerings and services.

The benefits of embedded finance

Embedded finance is transforming the way businesses and consumers interact with financial products. In addition, it offers multiple benefits for both: businesses and customers. Here are some benefits of it.

Enhanced customer experience

Companies can offer a seamless and convenient user experience by embedding financial services directly into their platforms. Customers can then access financial services on the same platform, eliminating the need to repeatedly connect or switch between financial apps or websites. It simplifies the user journey and increases customer satisfaction.

Expanded revenue streams

For non-financial companies, embedded finance offers the possibility of generating additional income. Financial services such as payments, lending, or insurance can allow firms to earn extra income from transaction fees, interest, or other revenue-sharing business models. It can help firms to increase profitability and capture a larger share of the customer’s wallet.

Improved access

Embedded finance can significantly improve access to financial services. It is particularly relevant for underserved and unbanked populations. Integrating financial services into widely used platforms makes it easier for people to gain access to banking, payment, or lending services, even if they do not have a traditional bank account. This democratization of financial offerings can foster financial inclusion and enable more people to participate in the digital economy.

Personalized and data-driven solutions

Embedded finance allows companies to use the data from their platforms to provide personalized financial solutions. These solutions are delivered by analyzing user behavior and transaction data. The functionality lets companies offer targeted financial products or services that meet their customer’s needs and preferences.

This data-driven approach allows for more accurate risk assessment and the definition and delivery of personalized pricing and offers. As a result, both companies and customers achieve better results.

Faster time to market and agility

Embedded financial instruments let you avoid building financial infrastructure from scratch. This results in significant savings in time and money. Non-financial firms can benefit from the expertise and infrastructure of specialized fintech firms or banking-as-a-service providers and thus quickly start providing financial services.

Flexibility makes it easier for firms to adapt to market needs, offer new propositions, and evolve in response to customer feedback.

Banking as a Service in real life

The best way to understand BaaS is through an example. Imagine you have a successful e-commerce platform called “Shopy” that sells various products online. You face intense competition and want to build customer loyalty.

You can expand your offering by embedding financial services, e.g., a more integrated and seamless banking experience for your customers. Moreover, rather than directing customers to external banking portals or requiring them to use separate banking applications, Shopy can use BaaS to provide banking services on its platform.

In partnership with BaaS, Shopy improves the customer experience by offering a one-stop solution that enables the seamless embedding of financial services into its platform. Customers can conveniently and securely make payments, access lending options, and manage their finances – all within the Shopy ecosystem.

This is just one of many examples of embedded financial services. There are many ways in which non-banks tech companies can improve the user experience and increase their revenues by offering more advanced and convenient financial services.

FAQ:

What is meant by Banking as a Service?

Banking as a Service (BaaS) involves a comprehensive process utilized by digital banks and third-party entities. The main goal of it is to establish a connection between their business infrastructure and a bank’s system through APIs.

This connection allows digital banks and third parties to offer embedded financial products in nonbank business lines directly.

What is an example of Banking as a Service?

There are many different examples of how BaaS can be used to embed financial services in businesses. Let’s go through some of them.

Green Dot Corporation and Apple.

Green Dot, a financial technology company, provides Apple’s BaaS solutions for Apple Cash. Through BaaS, Apple can offer its customers a virtual payment card, person-to-person wire transfers, and other banking features directly through the Apple Wallet app.

By partnering with Green Dot’s BaaS platform, Apple can enhance the Apple Pay user experience by providing seamless and integrated financial services.

Uber and GoBank

Well-known platform Uber has teamed up with BaaS provider GoBank to offer financial services to its drivers.

Thanks to this cooperation, Uber drivers can register for GoBank accounts. These give them instant access to their earnings, a debit card for expenses, and other banking features.

By integrating GoBank’s BaaS capabilities, Uber has improved the financial well-being of its driver partners by offering convenient and customized banking services on its platform.

Shopify and Stripe

To provide financial services to customers, an e-commerce platform Shopify has integrated Stripe’s BaaS capabilities.

With Shopify’s partnership, e-commerces can benefit from features: payment processing, fraud prevention, and financial reporting directly within the Shopify platform.

Stripe’s BaaS infrastructure enables Shopify to provide embedded financial services, allowing businesses to manage their transactions and finances more efficiently.

BBVA Open Platform and Prosper Marketplace

BBVA Open Platform, the BaaS arm of BBVA, partnered with an online lending platform Prosper Marketplace to provide financial services to Prosper’s borrowers.

Thanks to this partnership, Prosper borrowers can access loan origination, disbursement, and repayment directly on the Prosper platform.

What is the difference between BaaS and open banking?

The main difference is their purposes.

BaaS focuses on enabling non-bank businesses to integrate banking products and services into their offerings, however, open banking aims to provide access to bank data through APIs to third-party service providers.

Open banking allows providers to develop customized products and services based on customer banking data. Therefore, it is important to note that third-party service providers can only use customers’ banking data with their explicit consent.

For example, a financial management app can take advantage of open banking by integrating APIs, consolidating multiple accounts into a single dashboard, and providing a holistic view of a customer’s financial information.

Another example is a tool, which utilizes open banking to streamline the onboarding process at checkout.

In this case, customers are directed to their online banking login to verify details. It helps to enhance security, reduce fraud, and improve the efficiency of the checkout process.

📚Read more: Customer Onboarding

What is the difference between Banking as a Service and Banking as a Platform?

While both Banking as a Service (BaaS) and Banking as a Platform (BaaP) offer valuable solutions for businesses, they differ.

BaaS:

Primarily provides integrated banking services to non-bank corporate customers. More suitable if your goal is to enhance customer service.

BaaP:

Primarily serves the customers of traditional banks by integrating fintech services into the bank’s offerings.